It’s easy to get tripped up by assumptions when valuing a business, especially if you’re in a hurry to produce results. That’s why performing the right sense-checks can help you determine accurate valuations.

Our experts came together to discuss what they believe are the most useful sense-checks to help ensure accurate company valuations.

We hope you find these useful, and check back in soon for more content like this as we’ll be exploring additional ways to improve your valuations.

1. Avoid a hockey stick forecast

Your growth forecast shouldn’t look like a hockey stick… generally speaking. Ensuring that your financial forecast makes sense is top of our list of checks.

We’re dealing here with one of the primary valuation methodologies—the Discounted Cash Flow (DCF) method. Hockey stick-like growth in your DCF projections may indicate these projections are not realistic.

A useful tip is to check for consistency between the forecast margins and historical margins—EBITDA margin, EBIT margin, and Net Income margin. By checking that the forecasts actually reasonably match up to what was achieved in the past, you can at least assure that your forecasts are structurally similar to the real-world conditions that the business currently faces.

There needs to be a really good reason for such a large increase in margins… and usually the reason isn’t quite good enough.

2. Perpetual growth rate too high

Again, in a DCF analysis – the one we mentioned above and favoured by academics and practitioners alike – when you project the future cash flows and discount them to determine what the business is worth, one of the most sensitive inputs to your overall valuation result is the final year—the so-called ‘terminal year’.

That is the year that represents all future years extending out into perpetuity (all theoretical future years of the company).

Because that figure contributes such a substantial portion of the overall valuation – it is often more than all the other years combined – you need to very carefully check the assumptions behind it (it can often be more than 70% of the final valuation result!)

One critical component of the terminal value is the perpetual growth rate.

The perpetual growth rate is an assumption of the annual growth rate until the end of time.

The most widely accepted assumption for the perpetual growth rate is that company’s country’s long-term inflation target, provided it does not exceed the country’s historical GDP growth rate. This is because otherwise, logically, as the company grows it will eventually grow bigger than the entire economy of its country, which obviously doesn’t make much sense.

So there’s a narrow margin within which your perpetual growth rate lies and makes sense, but small differences can have a big impact.

The rationale for using the long-term inflation target is that it assumes that the business has reached such a mature state that it is no longer increasing market share or expanding in any other way, but simply increasing sales prices (and free cash flow) in line with all other prices in the economy (i.e. inflation). For the UK, for example, the long-term inflation target is 2% whereas for South Africa it is 5%.

You can find the long term inflation rate on websites like TradingEconomics.com.

3. Compare operating metrics with peer companies

Well-loved by practitioners, a common way to value businesses quickly is through the ‘comps’ approach, wherein you compare the target company to other similar businesses, either in terms of what the similar business (or part of it) recently sold for (transaction approach), or how much similar peer companies are valued at as a whole, according to its market cap (i.e. the value of all its shares added up).

Selection of your so-called “peer group” in this type of valuation is thus very important and requires a lot of thought.

One critical check that is often overlooked, is to benchmark the operating metrics (such as sales growth, EBITDA or EBIT margins) of the peer companies, against the company you are performing the valuation on.

It’s usually a good assumption that companies that operate in similar industries, exposed to similar industry risks, should have similar operating metrics.

If some of the peers have wildly different operating metrics, then you should probably question whether these companies should be included, or at least try to understand why.

4. Don’t include too many transactions

![]()

Another way to value a company is through comparing how much similar companies sold for (wholly or in part) in the past, and using that as a comparison basis.

But finding comparable transactions can be more difficult than simply finding appropriate peers.

Our team has observed that there can be a tendency to try to find as many transactions as you get peers, or a similar number. But this is often a mistake, and something that you should watch out for.

It’s a mistake because you can end up with outliers—transactions that are not a good fit for your company, as a comparison point.

Basically, you want to focus on the quality of your comparable transactions, rather than the quantity.

It’s far better to have one or two really appropriate transactions, than 15 or 20 transactions that aren’t that relevant.

One thing that signals that a transaction is not an appropriate comparison is when a very small percentage was acquired. This typically happens as a follow up to an earlier transaction or in case of an investment rather than an acquisition. Transaction multiples are most useful for transactions involving a controlling stake being acquired (i.e. at least 50%) as that is typical of a private transaction.

5. Check for discrepancy between valuation methods

In an ideal world, the different valuation methods should give similar results… in theory…although in practice this doesn’t always happen.

If there are major differences between estimations from different valuation methodologies, it may mean that some assumptions need adjusting.

For example, if the DCF is delivering a valuation that is 2x or 3x that of the comparable company approach, this could indicate that the discount rate used may be too low, or the discount applied to the observed multiples may be too high.

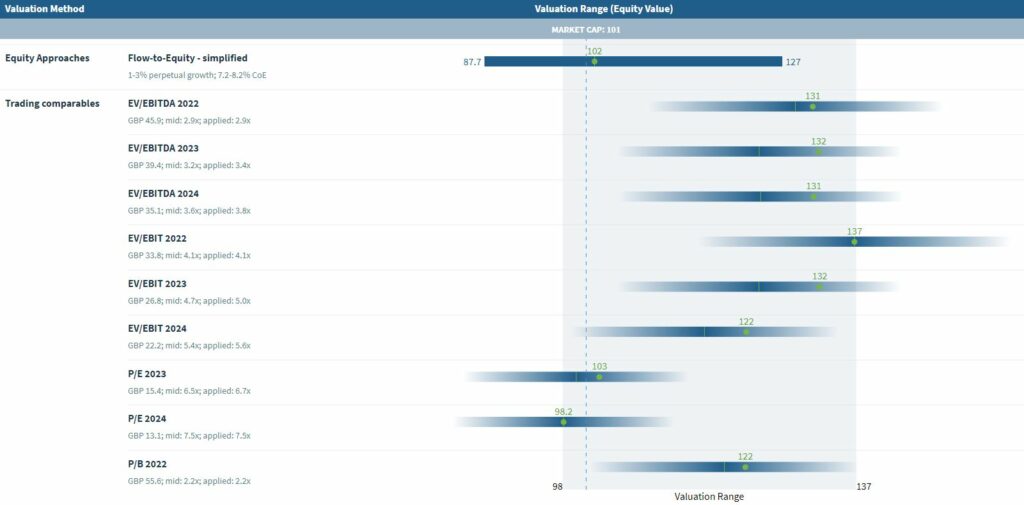

One very important check at the end of your valuation process is to see that the various methodologies speak to each other. A football field chart such as the one shown below is very useful for such a check:

If there are vastly different results you might want to double-check your key assumptions to find out what has gone wrong, or make sure you understand the reason for the difference.

Ultimately, of course, you are not using every valuation method, just the ones that fit the purpose for that type of company and your particular scenario. But it’s important to understand why differences have arrived between the pertinent methods so you can ensure your final results are valid.

Valuing a business is a precise exercise that warrants lots of checking and double-checking of assumptions. We hope you found our experts’ most recent guidance on this topic useful and that it allows you to conclude your business valuations with the confidence that the results make sense.

If you want to learn more about valuations, we offer a valuation course. Please get in touch to request a brochure – we’ll email it to you straight away.

Or if you already perform valuations regularly and you don’t yet have a subscription to Valutico, obviously we strongly recommend you book a demo to see how we can help you drastically improve the speed at which you deliver accurate, defensible valuations.

Of course, if you just want a one-off valuation, then we also can help with that.